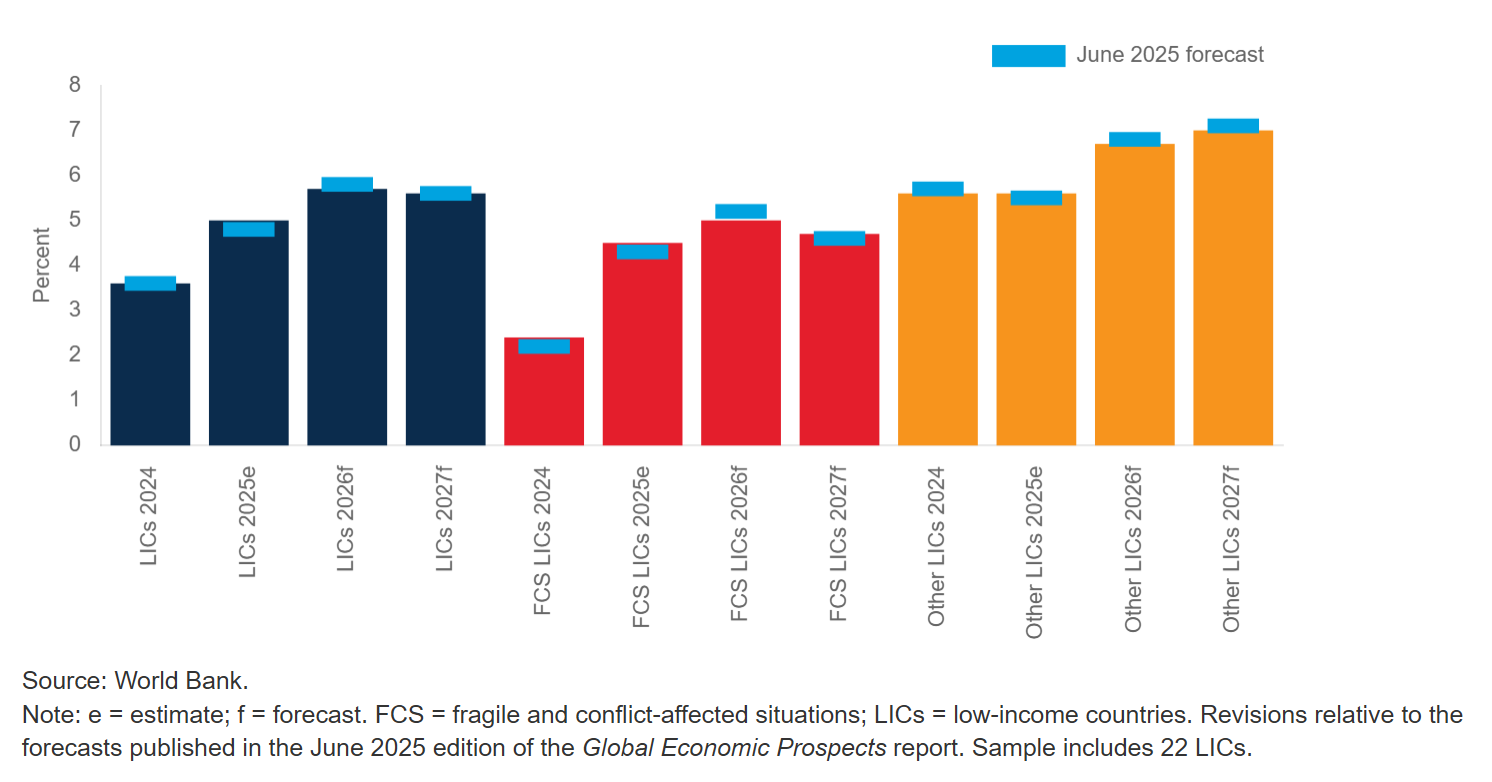

Low-income countries (LICs) have shown notable resilience in recent years. Despite heightened trade tensions and policy uncertainty, persistent conflict, and extreme weather, activity firmed last year, in some cases surpassing expectations (figure 1). Aggregate growth in LICs rose to about 5 percent in 2025, up from 3.6 percent in 2024, supported by easing conflict intensity in some countries, higher government spending, and favorable prices of key commodity exports — particularly coffee, gold, and other precious metals. The January 2026 Global Economic Prospects report offers a detailed analysis of recent developments and the economic outlook for low-income countries.

Figure 1. Growth forecasts compared with June 2025 projections

Fragility and conflict continue to shape economic performance

Fragility and conflict remain key differentiators of economic performance, with growth in LICs facing fragile and conflict-affected situations (FCS LICs) lagging that in other LICs. Although the baseline assumes some de-escalation of conflict in several LICs, the incidence of conflict remains elevated compared with pre-pandemic trends (figure 2).

Persistent conflict and insecurity disrupt production, discourage investment, limit the mobility of people and goods, and divert scarce public resources toward emergency and security-related spending and away from key development goals. These pressures can also weaken institutions and erode the effectiveness of policy measures designed to stabilize economic conditions and support recovery.

Even where the intensity of conflict eases, economies emerging from it often face deep scars - damaged infrastructure, eroded human capital, weakened administrative capacity, and heightened uncertainty. The result is that growth in FCS LICs tends to be well below that in other LICs, with recoveries that are weaker and more prone to be derailed by additional shocks.

Inflation is easing, but food insecurity remains acute

Inflation pressures have continued to ease, offering some welcome relief after a period of notable price spikes. Median headline inflation declined markedly over 2025 — from about 8 percent in the early part of the year to around 5 percent in the second half — with inflation slowing in more than 70 percent of LICs (figure 3). This disinflation reflects moderating global energy and food prices, alongside improved agricultural conditions.

Nevertheless, easing inflation does not mean that pressures on households have abated. Food prices remain elevated relative to other consumer items. For poor households — who spend a large share of their budgets on food — this continues to strain living standards. Moreover, food insecurity remains alarmingly widespread. In 2025, nearly 130 million people in LICs, about 20 percent of the total population of these countries — experienced crisis-level food insecurity or worse.

Firmer growth but limited dividends

Looking ahead, growth in LICs is projected to increase further to 5.7 percent this year, before easing slightly to 5.6 percent in 2027. This improvement is expected to be supported by moderating inflation, gradually strengthening domestic demand, continued reform momentum in some countries, and a gradual recovery of activity in environments where security conditions stabilize. Yet the development dividends from this growth will remain limited. Real per capita income growth in LICs is projected at about 2.8 percent per year in 2026–27 — an improvement, but still too slow to generate substantial reductions in extreme poverty or to provide enough productive jobs for rapidly expanding labor forces. In all LICs, real per capita incomes in 2027 are expected still to be about 5 percent below levels projected before the pandemic, with FCS LICs lagging even further behind (figure 4).

About 160 million youth — 20 percent of the current LIC population — will reach working age in LICs over the next decade. This makes the creation of productive jobs an urgent challenge. The share of the youth population (ages 15–24) is considerably higher in LICs than in other emerging market and developing economies (EMDEs). Moreover, in LICs, the number of young people not in employment, education, or training is estimated to have risen by nearly 20 percent between 2016 and 2025, while it declined in other EMDEs. With more than half of their population living in extreme poverty, only limited improvements in average living standards are expected in the next two years.

Moreover, rising debt burdens and borrowing costs have narrowed fiscal space in many LICs, while external financing is becoming more difficult. The scaling back of official development assistance in recent years has reduced an important source of financing for many LICs. With fewer external resources and higher financing costs, governments face increasingly difficult trade-offs: they must maintain fiscal sustainability through restraint and improved efficiency in public spending, while protecting and expanding growth-enhancing expenditures. Navigating these trade-offs will be a critical policy challenge in the years ahead.

Downside risks dominate, but policy action can shift the trajectory

The balance of risks to the LIC outlook remains skewed to the downside. Growth could be weaker than projected if conflicts persist or intensify, weather shocks become more severe, or global growth prospects deteriorate. Lower-than-expected commodity prices would weaken fiscal revenues and external balances in commodity exporters, while tighter global financing conditions or bouts of financial market stress could raise borrowing costs and limit market access.

Still, there are reasons for optimism. A more sustained easing of inflation, stronger domestic demand, and improved security conditions could support better-than-expected outcomes. But realizing these possibilities and translating growth into durable improvements in living standards will require determined policy efforts to address longstanding structural constraints, including expanding the stock of physical capital, accelerating human capital development, easing financing constraints, and strengthening institutions and governance frameworks.

The challenge for LICs is not simply to grow faster, but to grow in ways that generate jobs, reduce poverty, and strengthen resilience. The payoff to doing so is substantial: a more stable, inclusive, and durable development path – better aligned with the aspirations of the people across the world’s poorest economies.